The White Paper and FTA prospects for the UK and US

The White Paper released by the UK Government on 12 July 2018 deals primarily with the UK’s relationship to the EU. In keeping with previous statements and papers, it seeks a deep and comprehensive free trade agreement with the EU. But it also sets out the UK’s ambition to develop its own independent trade policy vis a vis the rest of the world. That includes signing Free Trade Agreements (FTAs) with other partners. The paper specifically mentions the US, Australia and New Zealand.

US or them?

But in comments made to the press on the occasion of his state visit to the UK, US president Donald Trump claimed that the White Paper would “kill” any chance of a trade deal with the US. He was not specific as to why he thought this was the case, and subsequently seemed to tone down his rhetoric. But looking beyond the bluster, what is it about the White Paper that might make striking an agreement with the US, or indeed any other trade partner, difficult?

Two of the key commitments made by the White Paper are: to mirror the EU’s customs arrangements vis a vis the rest of the world, including on rules of origin (the criteria that determine whether products are eligible for preferential treatment under a FTA); and a commitment to a “common rulebook” approach on regulation for a certain number of sectors in which cross-border trade with the EU (including Ireland) is important. There is an economic reason for these commitments: the UK wishes to avoid disrupting supply chains that span the EU and the UK through costs associated with customs and regulatory compliance. These supply chains are important to trade between the UK and EU, but also to the global competitiveness of both.

There is also a political imperative: the need to avoid introducing border measures between Ireland and Northern Ireland, in order to preserve the achievements of the Good Friday agreement.

The White Paper’s positions on customs and on regulation are likely to constrain how far trade partners find negotiating with the U.K. an attractive prospect. The regulatory issue is particularly important for dealings with the US (see here for a more in-depth treatment). This is because tariffs between the U.K. and the US are already low or zero in many of the goods that are traded by the two. The main measures factors affecting the trade costs are divergences in regulation between the EU (to which the UK seeks alignment) and the US.

That is also true in areas like agriculture where tariffs are higher. Here the application of the precautionary principle has been an obstacle to US exports to the EU. A prime example of this is beef, which was the object of one of the longest-running disputes between the US and the EU at the WTO.

Finally, the issues are also likely to arise in key services areas, notably financial services in which the White Paper calls for a specific set of arrangements, including on regulation. Audiovisual services are another area in which regulatory frameworks differ substantially between the EU and the UK, on one hand, and the US on the other.

The regulatory divergences between the EU and the US were one of the sticking points in the now-suspended negotiations Transatlantic Trade and Investment Partnership (TTIP) between the EU and the US. The differences are not simply in the minutiae, but in the overall architecture of regulation. In particular, the EU holds to the precautionary principle as a matter of treaty law. Under this approach, member states have the ability to regulate even when the scientific evidence is unclear. The US holds to a risk-based approach that places a greater burden of proof on regulators to justify their approach based on science.

The economic and political factors referred to above drive the White Paper’s aim for regulatory alignment with the EU. While this is meant to be partial – i.e. to the extent needed not to create supply chain frictions or a hardening of the Irish order – it is likely to affect sectors of economic and political interest to the US (and other partners such as Australia). Moreover, exactly how partial is unclear, and this ambiguity is not good think for businesses looking to take advantage of FTA opportunities. President Trump is therefore correct in his assessment that the UK will probably need to choose between deep integration with the EU and deep integration with the US.

Deep calls to deep

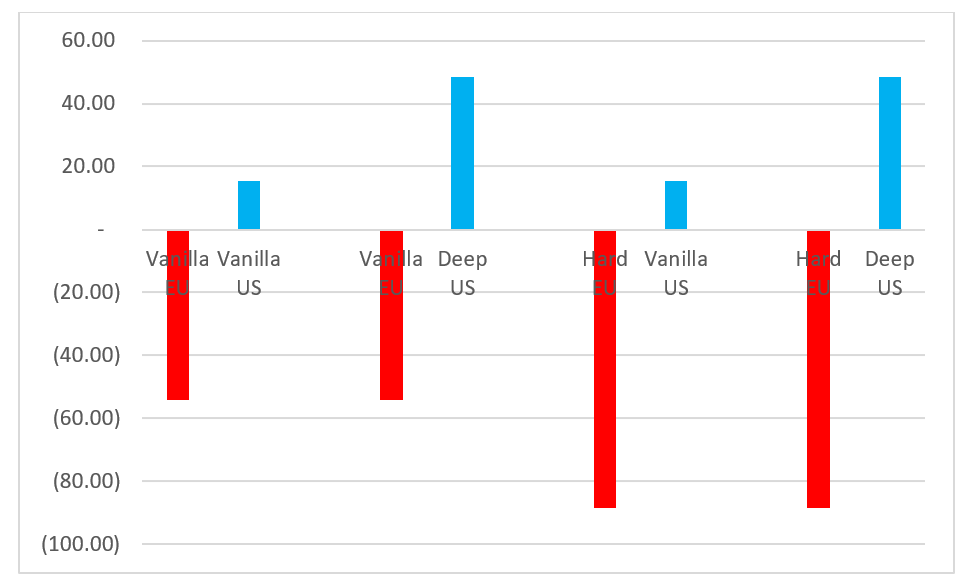

Given the choices, what should the UK do? From a purely economic point of view, maintaining deep integration with the EU as a policy priority is sensible. To see this, we model the effects of alternative forms of FTA between the UK and, respectively the EU and the US. For the UK’s relationship with the EU, we look at a scenario in which the UK leaves with no deal at all (“hard”) or reverts to a deal of the sort the EU currently has with non-EU members such as Canada or Korea (we label this a “vanilla” agreement). The latter is the sort of arrangement thought to be favoured by the likes of David Davis. For the UK’s relationship with the US, we look at a scenario in which the UK negotiates a “vanilla” agreement with the US, or a “deep” agreement, which involves much more substantial liberalisation and regulatory convergence, of the sort observed within the EU’s single market.

Figure 1 below presents the results, using a gravity model of trade, which is generally recognised by trade policy specialists as a key part of sensible trade modelling. The red bars give the losses to the UK associated with moving from current arrangements to a vanilla deal with the EU or hard/ no deal exit. The blue bars give the gains associated with either a vanilla or a deep agreement with the US.

We see that in no arrangement does a FTA of any depth with the US offset the losses of moving away from deep integration with the EU. Even if the UK were to negotiate a Canada-style FTA with the EU and negotiate a deep one with the US, it would still face some (small) losses. Note that even this is on the extremely optimistic assumption that the UK could negotiate and implement – on the point of leaving the EU- an agreement with US of the sort that has not been see outside the European Economic Area, the rules of which took decades to negotiate. Moreover, negotiating such a deep agreement would involve substantial changes to public and regulatory policy, and it is questionable, to say the least, how much appetite there is for this.

President Trump is probably correct is his assessment that the White Paper aligns the UK with the EU and that negotiating with the UK under these circumstances would resemble negotiations with the EU, albeit “in miniature”. But the economics suggests that the White Paper has got that call right. The economics also suggests that the UK is unlikely to be able to secure deep integration with the EU and pursue deep integration with the US independently of the EU. This in turn suggests that if the UK really did want to pursue a FTA with the US in a gainful manner, it would probably have been better off – ironically – staying within the EU and prodding the EU in that direction.

Finally, this episode reminds is that modern day FTAs are about deep institutional reforms. These extend well beyond the remit of trade policy as traditionally conceived, and touches on a variety of subjects including social preferences to risk and regulation. There may be reasons of political philosophy that lead people to incline towards the US rather than the EU. But if that is the case, then these reasons should be expressed as such and not disguised as economics. And they should be set against economic factors, as well as other political factors, such as the Irish border question.