What moves on Free Movement?

Along with the Irish border, the question of free movement was one of the seemingly intractable questions at the recent EU summit in Salzburg. Put simply the EU does not want to convey the impression that it is possible for the UK – or any other member -to give up a commitment to this key principle of the single market and retain the benefits that come from deep levels of market access in goods and services. The French minister for Economics, Bruno Le Maire put it like this: “Any decision that would give European citizens the feeling you can exit the EU and keep all the advantages would be suicidal, and we won’t make that decision”. That line of reasoning explains the EU’s hostility to the UK’s White Paper, or “Chequers”, position.

The UK government’s position reflected in the July White Paper seemingly accepts this, to an extent at least. The bargain it proposes is that the UK would exit the single market for services in return for it leaving single market rules on the movement of people. The reasoning behind this position may be that the UK’s strength in particular services sectors – financial services, professional services, information and communication sectors – would allow it to negotiate deep free trade commitments using principles that govern global services trade. And relinquishing the principle of free movement would help preserve one its “red lines” – “taking control” of immigration, which it believes is one of the key lessons from the June 2016 referendum.

The EU has expressed scepticism about this position, and the UK’s approach more generally. But what the EU and the UK have in common is that free movement is seen as a “price” that needs to be paid to secure market access in goods and services, and that a reluctance to pay that price means accepting a lower level of access. While this may have some truth politically, from an economic perspective, the logic is more than questionable. Indeed, we argue that relinquishing the principle of free movement carries its own economic price, through its effects on trade, and more generally on the competitiveness of firms that face higher search costs for skills. This in turn has implications for the way both the UK and the EU conduct their negotiations.

Free movement of people and trade

The principle of free movement gives EU citizens access to labour markets in all of the EU member states (as well as non-member states that have committed to this principle, such as the members of the European Economic Area, and Switzerland). From an economic perspective, there are many ways in which free movement reinforces trade.

One of these is through access to skills. The ability of workers to relocate freely can “thicken” labour markets, making it easier for businesses to match skills needs to their requirements. This helps businesses become more competitive, not just on a European scale, but on a global scale. Other effects include reducing trade-related transactions costs (e.g. through networks or through knowledge of local markets, preferences, and institutions).

Empirical research into the relationship between immigration and trade more broadly reveals that a positive impact on the UK’s trade. An econometric analysis estimated that a 10% increase in immigration from non-commonwealth countries is estimated to increase long-run exports by 5%. The effect for non-commonwealth countries is much stronger than for commonwealth countries, and reflects in part the impact of immigrants from Europe.[1] The findings on the export response to immigration is consistent with findings for Spain[2], the US[3] and Canada[4].

One very specific link between trade and free movement is found in the realm of services. One of the modes through which services are supplied on a cross-border basis is through the movement of a service supplier (e.g. an architect or a lawyer) from one country to another. Another mode is for businesses to set up a commercial presence (e.g. the branch of a bank or an office) in another country. But to make most of the ability to do this, businesses need to be able to recruit and move employees across borders. Importantly, countries may reduce or lift restrictions on the movement of workers in this manner without committing to free movement per se. But committing to free movement is the simplest way of doing away with these restrictions across all sectors.

The costs of losing free movement on service trade

Restrictions to services trade are difficult to measure quantitatively. One way of doing this is through restrictiveness indices, that score services sectors by country. The OECD has computed such indices for its members. Among the factors that influence the overall score awarded to a sector in a country is the extent to which it allows for the movement of people to supply services.

We can therefore use indices measured for EU countries to see how much scores change if the UK were to rescind its commitment to free movement vis a vis EU members states, and vice versa. We can also measure how sensitive bilateral flows of services trade between the UK and EU member states are to changes in restrictiveness indices, using a gravity model of trade. Putting the two together gives us an estimate of the impact of moving away from free movement. The estimates are partial: they are limited to services (access to skills is clearly important to goods trade), and they do not capture the full extent to which free movement affects the supply of services, since the restrictiveness indices capture measures that affect service trade specifically and not all factors that affect the competitiveness of services sectors. Nevertheless, the results provide a good first indication of the effects of losing the commitment to free movement.

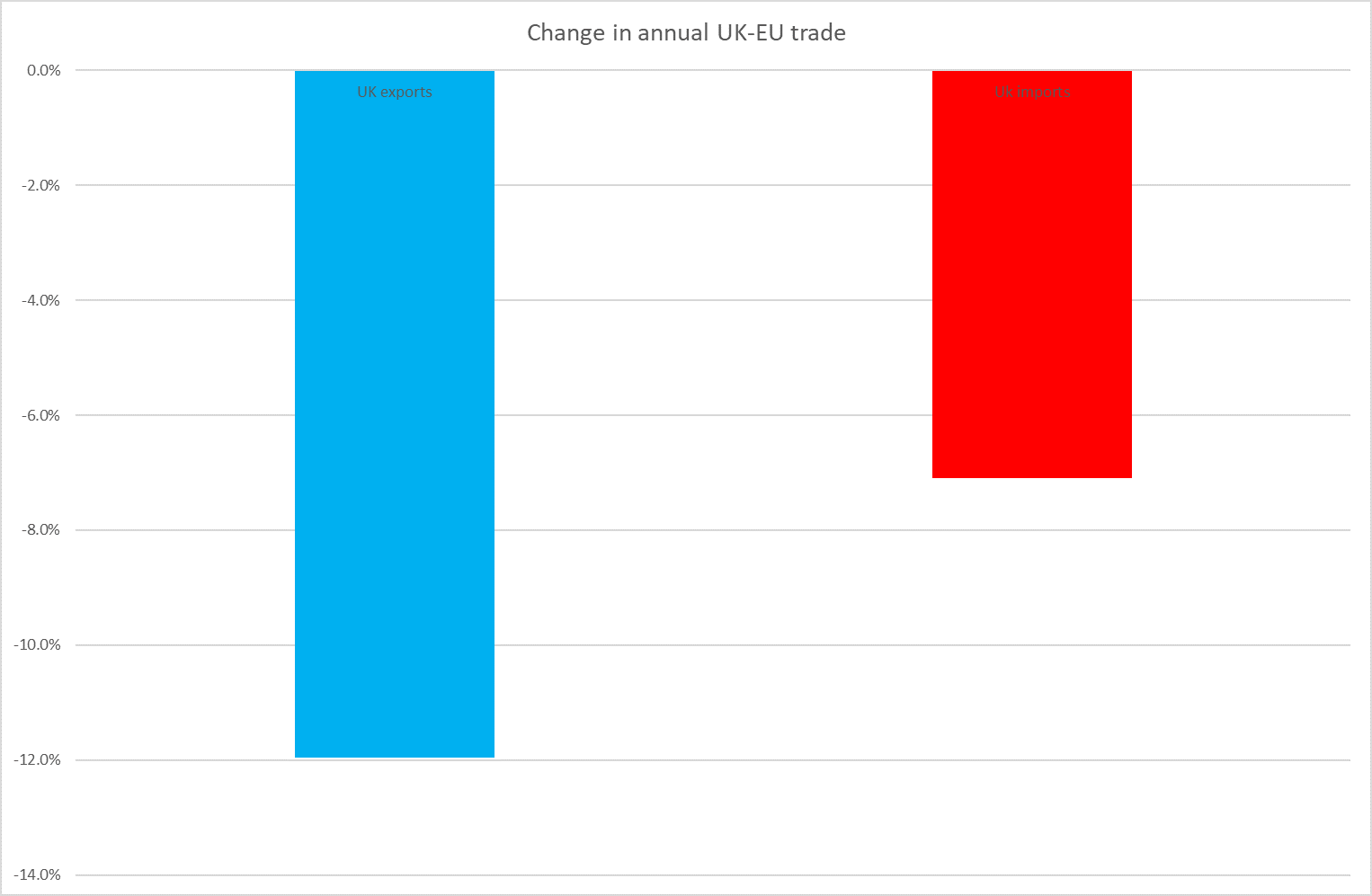

Figure 1 shows the overall impacts on UK services exports to the EU and services imports from it.

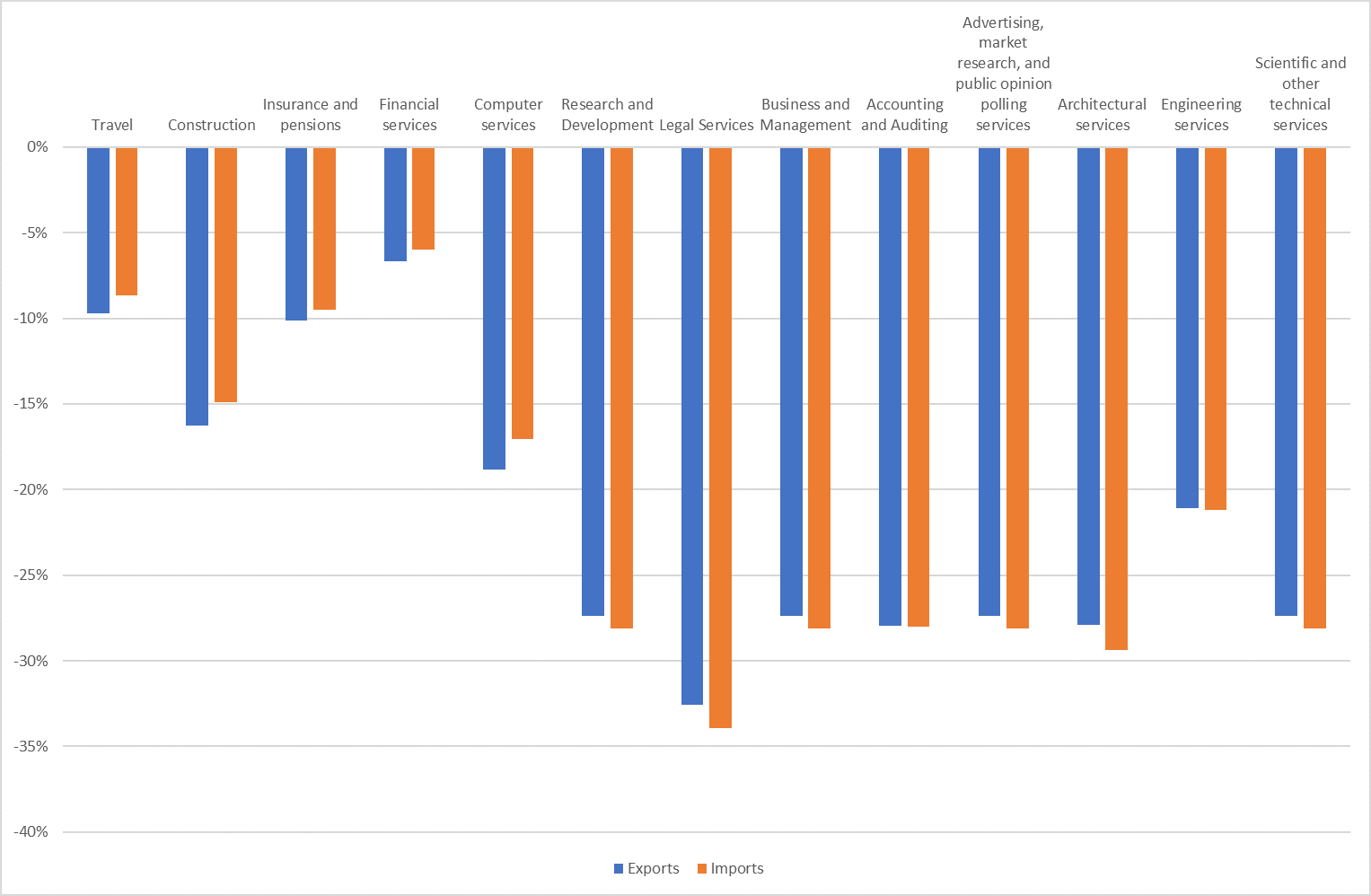

Figure 2 reports results for some specific sectors.

The effects are particularly strong in the professional services sectors (law, accounting, business services), and knowledge-intensive sectors such as computer services and research and development. The result is intuitive, given the importance to these sectors of hiring skilled employees, and deploying them efficiently across offices.

We also observe that that though overall, the effects on UK services exports dominate imports from the EU (figure 1), the effects on professional services is comparable. This probably reflects the growing (though still incomplete) interconnectedness of professional services sectors across the EU.

The figures probably understate the overall impact on UK services trade. This is because they capture EU-facing trade effects, and not global impacts. Yet UK services are globally competitive, and losing access to skills will affect that global level of competitiveness. For example analysis conducted by Frontier Economics for the Royal Institute of British Architects suggests that 7% of UK architecture exports to non-EU markets could be in jeopardy if UK businesses were constrained in their access to EU skills. This is lower in percentage terms than the loss in EU-facing trade – but is significant nevertheless given that upto 85% of architecture exports go outside the EU.

What ways forward?

The results suggest that both the UK and the EU have an inherent interest in reaching an agreement on the issue of free movement, not least because of the wider effects this has on trade. As observed above, the UK’s proposal is that it exit the single market for services, in return for it being allowed to relinquish the principle of free movement. The logic for this is not economic: it reflects a political decision based on an interpretation of the June 2016 referendum.

But exiting the single market does not mean abandoning free trade in services. Indeed, the UK’s proposal spells out the need to reach deep commitments on services trade. That could be done using the legal framework for services trade developed through the WTO’s General Agreement on Trade in Services (GATS), and built on in free trade agreements that use this as a model. That framework allows for general and sector-specific commitments.

Crucially, the framework allows for commitments on liberalising the movement of people for the purposes of supplying services. This is not the same as free movement – the latter guarantees general access to labour markets. But deep commitments on the movement of people could mitigate the negative impacts quantified above And because this is done under the heading of trade law governing services, it can be handled separately from the more emotive discussion of immigration policy.

Of course, the question remains whether such an approach can be negotiated politically. The EU has long held the position that the four freedoms of the single market are indivisible. As already explained, there is are sound economic grounds for considering these different freedoms as reinforcing each other. But to insist that deep commitments in, say, services must depend on free movement is more a case of dogma than logic.

Moreover, the loss of free movement as currently enshrined in the EU single market will have costs over and above the ones identified in the modelling. In particular, businesses in the UK will face an increase in search costs for skills. Whereas under current arrangements, a computing or architecture business in London or Manchester could attract job applicants from Paris, that may not be as easy in a new arrangement where commitments are made for the provision of services, rather than to provide reciprical access to labour markets

As explained elsewhere, the EU’s position is probably informed by a fear that if it were to allow one country to selectively opt in to certain types of commitment, then it would need to allow this for others. But as the results we have reported show, losing free movement carries its own price in terms of its impact on trade and competitivenes. Free movement should not therefore be viewed as a price to be paid for trade liberalisation, either by the EU or the UK. If the UK chooses to relinquish the principle of free movement, it will be jeopardising its own competitiveness, even if it were to negotiate deep levels of market access. From an economic perspective, there is little sense in the EU telling the UK “you can’t hope to get existing levels of market access without free movement” as if this was a form of free riding: the UK will have already have diminished the ability of its businesses to take advantage of the competitive opportunities created by better access.

On a more positive note, the architecture for negotiating commitments to free movement for the supply of services (principles that could also be extended to goods) is well understood, and both parties have an interest in minimising negative effects on trade. There is thus an opportunity for both the UK and the EU to dispense with the more emotional rhetoric and dogma that has clouded the possibility of an agreement, and to find common ground.